Research Foundation

The academic literature behind our trading strategies

Research Foundation

Overview

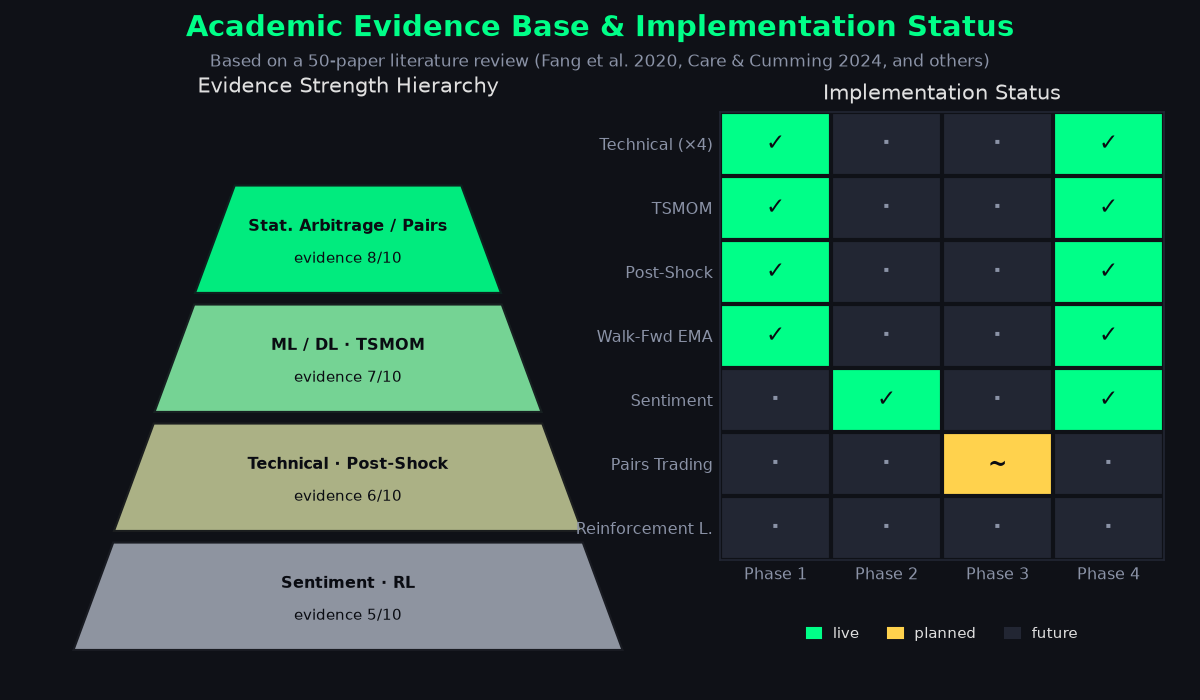

This system is grounded in peer-reviewed academic research on intraday cryptocurrency trading. Rather than chase whatever indicator is fashionable, each implemented strategy traces back to a published result with a measurable effect size. The literature suggests a rough evidence hierarchy: algorithmic / statistical arbitrage (≈8/10) > machine learning (≈7/10) > technical analysis (≈6/10), with transaction-cost modelling repeatedly flagged as the difference between a paper edge and a real one. The sections below summarise the key findings per strategy class and how each maps into the live system.

1. Intraday Momentum (TSMOM)

Key Finding

Shen et al. (2021) and Borgards (2021) document strong intraday momentum in Bitcoin and across 20 cryptocurrencies:

- The first 30-minute volume spike of a session helps predict its direction.

- Profitable momentum windows are larger than in equity markets.

- The effect is attributed to noise traders and the lack of a consensus fundamental valuation for crypto assets.

Implementation in This System

The TSMOM strategy votes in the direction of recent intraday returns, scaled by move strength, on the 1h timeframe — and the reweighting engine boosts it in trending (BULL/BEAR) regimes where continuation is most reliable.

References

- Shen, D., Urquhart, A., & Wang, P. (2021). Intraday momentum in the cryptocurrency market. International Review of Financial Analysis, 75, 101745.

- Borgards, O. (2021). Dynamic time series momentum of cryptocurrencies. The North American Journal of Economics and Finance, 57, 101428.

2. Post-Shock Mean Reversion

Key Finding

Miralles-Quirós & Miralles-Quirós (2022) and Wen et al. (2022) find:

- Profitable overreaction after negative price shocks.

- The reversal materialises roughly 6–24 hours after the shock.

- Positive shocks do not yield reliable reversals — the effect is asymmetric.

- Mean reversion is stronger during periods of liquidity constraint.

Implementation

The Post-Shock Reversal strategy fires a BUY after large downside shocks and deliberately stays flat after upside shocks, mirroring the documented asymmetry.

References

- Miralles-Quirós, J.L., & Miralles-Quirós, M.M. (2022). Intraday momentum in cryptocurrency markets. Finance Research Letters, 44, 102105.

- Wen, F., Xu, L., Ouyang, G., & Kou, G. (2022). Retail investor attention and stock price crash risk. International Review of Financial Economics, 65, 101537.

3. Walk-Forward EMA & Volatility Targeting

Key Finding

Tzouvanas et al. (2020):

- EMA crossover strategies limit drawdown versus buy-and-hold.

- Walk-forward optimisation prevents overfitting a single static parameter set.

- Including transaction costs is mandatory — even 0.1% per trade erodes the edge.

- Volatility targeting (scaling position size by 1/σ) stabilises risk.

Implementation

The Walk-Forward EMA strategy re-fits its EMA parameters on a rolling window and sizes positions inversely to volatility, with MEXC fees modelled explicitly.

References

- Tzouvanas, P., Kizys, R., & Tsend-Ayush, B. (2020). Momentum trading in cryptocurrencies: Short-term returns and diversification benefits. Economics Letters, 191, 108728.

4. Algorithmic Arbitrage & Statistical Pairs Trading

Key Finding

Krauss (2017), Care & Cumming (2024), and Addy et al. (2024):

- Statistical arbitrage shows the strongest consistent edge in crypto (≈8/10).

- Pairs trading via cointegration (Engle-Granger) exploits temporary spread dislocations between correlated assets.

- ML/DL methods are improving on classical pairs approaches.

- This class is planned for Phase 3 of the system (correlation + cointegration screening, then z-score spread monitoring).

References

- Krauss, C. (2017). Statistical arbitrage pairs trading strategies: Review and outlook. Journal of Economic Surveys, 31(2), 513–545.

- Care, R., & Cumming, D. (2024). Technology and automation in financial trading: A bibliometric review. Research in International Business and Finance.

- Addy, W.A. et al. (2024). Algorithmic Trading and AI: A Review of Strategies and Market Impact. World Journal of Advanced Engineering Technology.

5. Machine Learning & AI Approaches

Key Finding

Sun (2025), Meng & Khushi (2019), and Fang et al. (2020):

- ML/DL methods can outperform rule-based systems (≈7/10 evidence).

- An ANN + genetic-algorithm model has reported ~72.5% directional accuracy and ~23.3% return in intraday FX speculation (Evans et al. 2013).

- Reinforcement learning shows promise but overfitting remains the key risk.

- Transaction costs and slippage are critical to model correctly, or backtests flatter to deceive.

References

- Sun, Y. (2025). A survey of statistical arbitrage pair trading with machine learning, deep learning, and reinforcement learning methods. Working Papers.

- Meng, T.L., & Khushi, M. (2019). Reinforcement Learning in Financial Markets. Data, 4(3), 110.

- Fang, F. et al. (2020). Cryptocurrency trading: a comprehensive survey. Financial Innovation, 8.

- Evans, C., Pappas, K., & Xhafa, F. (2013). Utilizing artificial neural networks and genetic algorithms to build an algo-trading model for intra-day foreign exchange speculation. Mathematical and Computer Modelling, 58(7–8), 1249–1266.

6. Sentiment & Discourse Analysis

Key Finding

- Social-media sentiment leads crypto price by 1–2 days.

- Twitter/Reddit mood has measurable predictive power for returns.

- News sentiment from institutional sources (FT, Reuters, central banks) has a stronger, more durable impact than retail social media.

- The Fear & Greed index correlates with short-term reversals at sentiment extremes.

References

- Kraaijeveld, O., & De Smedt, J. (2020). The predictive power of public Twitter sentiment for forecasting cryptocurrency returns. Finance Research Letters, 35, 101445.

- Bollen, J., Mao, H., & Zeng, X. (2011). Twitter mood predicts the stock market. Journal of Computational Science, 2(1), 1–8.

Evidence Summary Table

| Strategy Class | Evidence Strength | Key Paper | Implemented |

|---|---|---|---|

| Statistical Arbitrage / Pairs | 8/10 | Krauss (2017) | Phase 3 |

| ML / Deep Learning | 7/10 | Sun (2025) | Partial |

| Technical Analysis | 6/10 | Fang et al. (2020) | ✅ Full |

| Intraday Momentum | 7/10 | Shen et al. (2021) | ✅ Full |

| Post-Shock Reversal | 6/10 | Miralles-Quirós (2022) | ✅ Full |

| Walk-Forward EMA | 6/10 | Tzouvanas (2020) | ✅ Full |

| Sentiment Analysis | 5/10 | Kraaijeveld (2020) | ✅ Full |

| Reinforcement Learning | 5/10 | Meng & Khushi (2019) | Phase 5 |

Figure 4: Academic evidence hierarchy and implementation status

Figure 4: Academic evidence hierarchy and implementation status

Research Gaps We Address

- Out-of-sample validation via the shadow portfolio

- Real transaction-cost modelling (MEXC 0% maker)

- Adaptive reweighting instead of fixed parameters

- Regime-aware strategy selection