Methodology

How the Bayesian fusion engine works

Methodology

1. Data Pipeline

- 10 cryptocurrency pairs on the MEXC exchange (BTC, ETH, SOL, BNB, XRP, DOGE, PEPE, WIF, SUI, AVAX)

- 5 timeframes: 1m, 5m, 1h, 4h, 1d

- OHLCV ingestion every 60 seconds

- PostgreSQL time-series storage with upsert deduplication

2. Strategy Layer

Eight independent strategies produce signals (BUY / SELL / NEUTRAL) with confidence scores in the range 0.0–1.0.

Technical strategies:

- RSI + MACD (momentum)

- Bollinger Bands (mean reversion)

- EMA Crossover (trend following)

- Volume Spike (volume confirmation)

Empirical strategies (academic evidence base):

- Intraday Time-Series Momentum (TSMOM)

- Post-Shock Mean Reversion

- Walk-Forward EMA with Volatility Targeting

Sentiment strategy:

- A composite score from the Fear & Greed Index, CryptoCompare news, crypto RSS feeds (11 sources), and macro feeds (FT, Fed, CNBC)

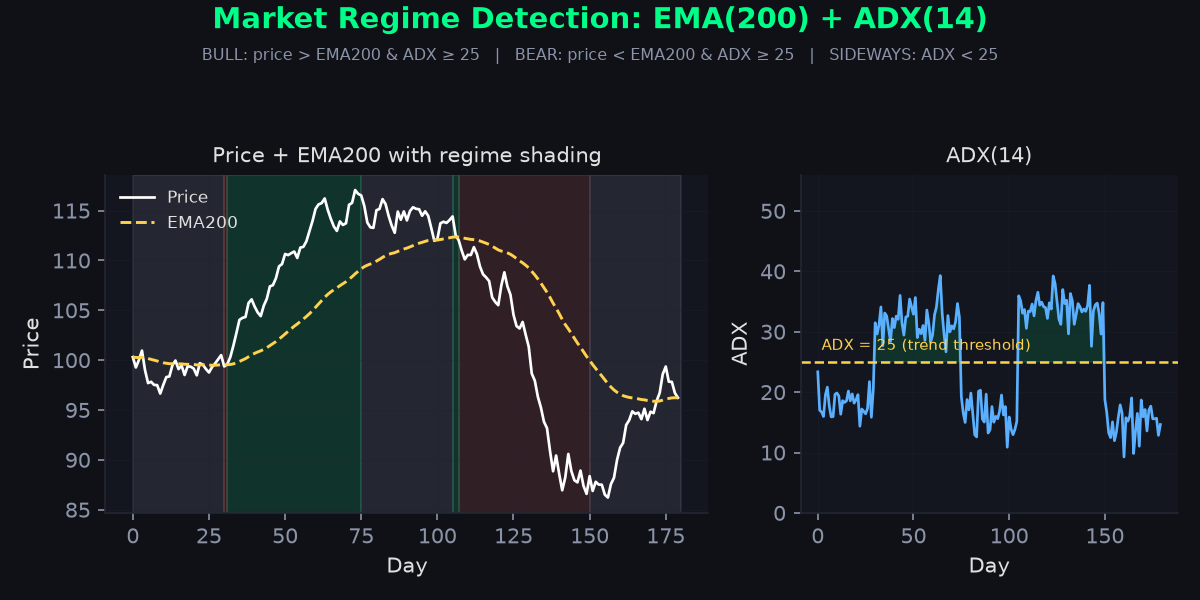

3. Market Regime Detection

Using EMA(200) + ADX(14) on daily candles:

- BULL: price > EMA200 and ADX ≥ 25

- BEAR: price < EMA200 and ADX ≥ 25

- SIDEWAYS: ADX < 25

The regime sets the Bayesian prior probability of an upward move, P(BUY):

- BULL → prior = 0.60

- BEAR → prior = 0.40

- SIDEWAYS → prior = 0.50

Figure 2: Market regime detection using EMA(200) + ADX(14)

Figure 2: Market regime detection using EMA(200) + ADX(14)

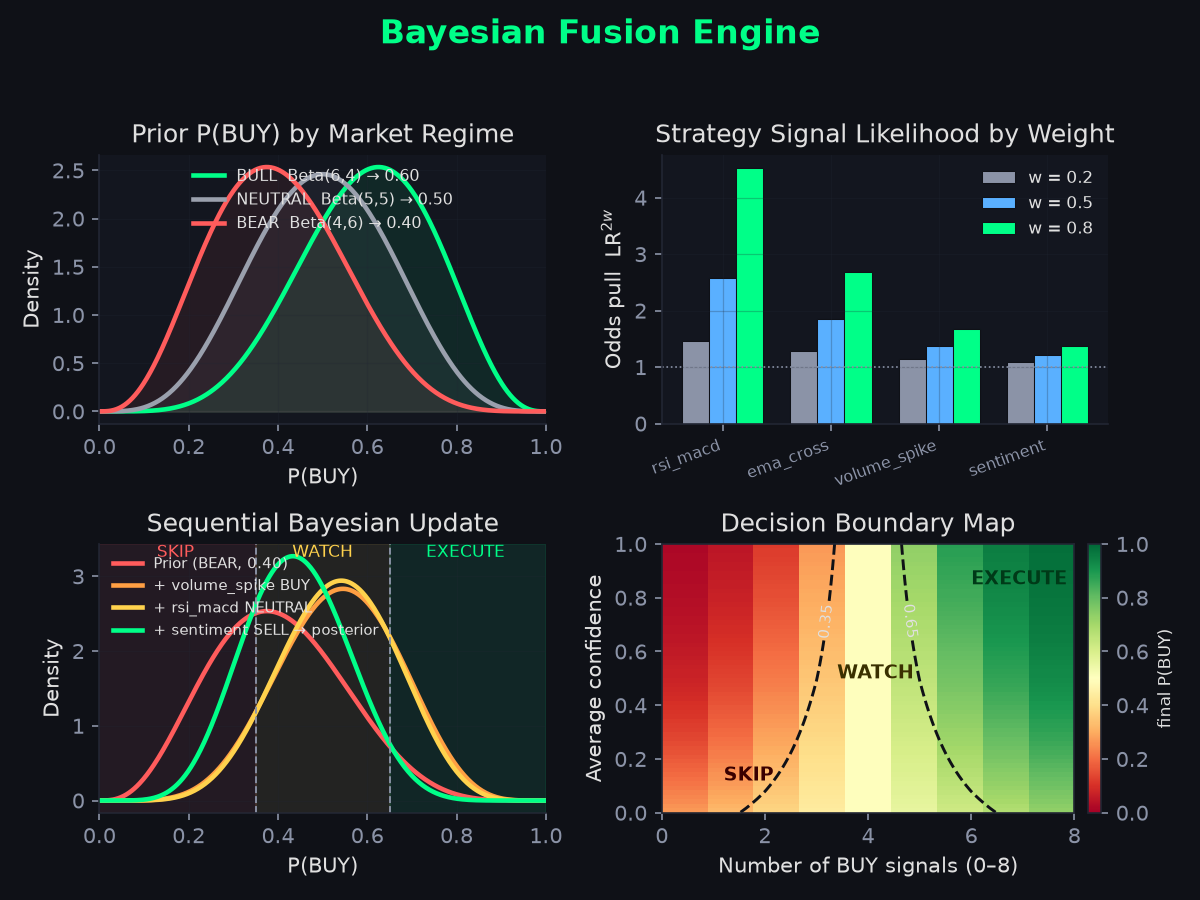

4. Bayesian Fusion Engine

The engine combines all eight strategy votes as a naive-Bayes product:

P(BUY | s1…s8) ∝ P(BUY) × ∏ P(si | BUY)^(2 × wi)

where wi is the reliability weight of strategy i, learned from historical

performance. The exponent amplifies high-reliability voters and damps the rest.

Decision thresholds on the posterior confidence:

- confidence > 0.65 → EXECUTE

- confidence 0.35–0.65 → WATCH

- confidence < 0.35 → SKIP

Figure 1: The four-panel Bayesian fusion architecture

Figure 1: The four-panel Bayesian fusion architecture

5. Adaptive Daily Reweighting

Every night at 02:00 UTC:

- Performance metrics are computed (24h and 7d win rate, Sharpe ratio).

- Market regime is detected per symbol.

- Regime multipliers are applied — momentum strategies are boosted in trending markets, mean-reversion strategies in sideways markets.

- Claude AI (Anthropic

claude-sonnet-4-6) analyses the performance data and recommends weight adjustments. - Final weights blend three sources: statistical (50%) + decay (30%) + AI (20%).

- The weights are persisted and applied to the next day’s fusion.

6. Shadow Portfolio

A $1,000 USDT paper-trading portfolio tracks system performance:

- Position sizing: 1% of portfolio risk per trade

- Stop loss: 1.5× ATR below entry

- Take profit: 3× ATR above entry (2:1 reward/risk)

- Transaction costs modelled: MEXC 0% maker, 0.1% taker

- No real money is traded

7. Blog Generation

Daily Alpha Brief posts are generated automatically:

- Data is extracted from the live database

- Claude AI writes the narrative sections

- The Hugo static site is rebuilt and deployed to Cloudflare Pages

- Posts are published at approximately 03:00 UTC daily